|

Updated

12/20/2010

WindFuels

Scale-up

The two most common

problems with most of the renewable energy ideas is either

they are not competitive or they are not scalable to the multi-terawatt

level. We don't just need an alternative solution that can

competitively produce a million gallons/year, but rather one

that can ramp-up to

tens of millions of barrels/day. Industrial ramp-up rates greater

than 20% annually are never easy to sustain more than a decade.

However, we’ve seen industrially driven scale-ups in

the past of greater magnitude than what is needed here, and

it can be instructive to reflect on some of the amazing past

successes – the automotive, aircraft, petrochemical,

television, computer, cell-phone, wind power, and drug industries,

to name but a few. Common denominators in the successes are

profitability within a reasonable time frame, constantly escalating

demand, and ample raw materials that can be easily exploited

and meet a continuously escalating demand.

In the Economics Overview,

we’ve shown that

WindFuels would be very profitable

in

a

short

time

frame.

One of the most important reasons for this is that there is a growing supply

of very cheap off-peak energy in regions of high wind penetration. As we show

on the Off-peak Wind page, and in a recent

article on Deployment, Off-peak

Wind energy will continue to be an

order of magnitude cheaper than CSP and most other renewable resources. Most

of the equipment needed for Windfuels is very similar to that which has been

used

in

the petrochemical industry for the past 60 years or more. It is cheap compared

to

what is needed

for algae oil or cellulosic ethanol because it doesn’t involve complex

cellular extractions.

As traditional crude production gradually diminishes

and must be replaced by more expensive and polluting fossil alternatives, there

is an assured demand

for scale up for WindFuels. We therefore need to assess

the feedstocks, then we’ll look briefly at the challenges which would be

faced by rapid scale-up.

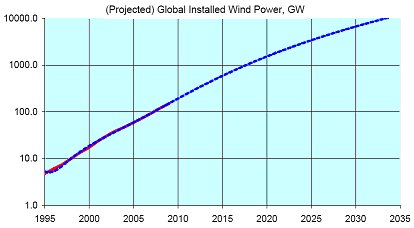

Cheap off-peak energy; the scalability of Wind.

The availability

of low cost energy will be influenced by the growth of the wind

power industry. Wind energy is clearly competitive, and it has

proven for the past 15 years that it is scalable, as shown here.

Installed (peak) wind energy projection based

on a fourth-order

fit to the data from the past 15 years.

|

As we

explain in detail on the off-peak

energy page, the RFTS plant

will simply connect to the grid in an area where projections

show a lot of clean off-peak energy. Doing so would provide

a market for off-peak wind energy and stabilize the grid for

the variability of

wind. This would enable continued growth of wind energy. (It

may be decades before a wind farm is installed

primarily to support an RFTS plant.) At least eight multi-billion-dollar

companies around the world (Vestas, Gamesa, GE Wind, Enercon,

Siemens, Clipper,

Mitsubishi, and Hyundai)

have demonstrated they can build and install multi-megawatt

wind turbines at a remarkable rate. As of late 2010, over

200 GW of peak wind power (about 70 GW of average power)

was installed worldwide.

The growth rate in wind energy has recently slowed – partly

because of the financial crisis and partly because of of the grid stability

challenges from the lack of a suitable energy

storage

solution. Energy storage, a primary obstacle to continued wind-energy

growth, disappears when the excess off-peak wind energy is converted to clean,

liquid fuels within a few hundred miles of the wind farm.

The steady drop in

prices seen in the three decades prior to 2006 ended for two years, but

it has recently returned. Additional manufacturing capacity has been added,

and

the economy-of-scale price reductions seen

over most of the last 20 years, have returned. Other large international

manufacturing companies (such as aircraft and truck manufacturers) will likely

enter the fray

as it becomes known that WindFuels will make wind energy a 70-year growth

opportunity.

The cost of wind turbines dropped 20% from early 2008 to late 2010. The levelized

mean cost of energy is now under $40/MWhr for wind, compared to $170/MWhr

for CSP and $220/MWhr for PV. Off-peak wind energy is becoming widely available

at under $12/MWhr in areas of high wind penetration.

One of the biggest obstacles to maintaining the

22% annual growth rate in wind energy has been that of power transmission

and grid connectivity. China has shown that high voltage DC (HVDC) is quite

cost

effective for electrical transmission over distances greater than 1100 km.

However, that still does not address energy storage issues, the transportation

sector,

or the cost of on-ramps to an HVDC grid – should it be built. These

primary obstacles to continued wind-energy growth disappear when the energy

is converted

to clean, liquid fuels within several hundred miles of the wind farm. There

is no doubt that wind energy can resume its phenomenal growth rate as soon

as the

new growth opportunities that WindFuels will create are appreciated.

Again, we should emphasize that the RFTS plant will be essentially independent

of both the wind farms and the CO2 separation processes at coal

power plants, though they will be connected through open markets. The WindFuels

plant will create an almost insatiable market for CO2. It will eventually

close the loop on CO2 and eliminate the need for carbon sequestration.

The largest component of the RFTS plant is the water electrolyzer. They initially

will be expensive, but their prices will come down quickly. We return to

each of

the key subsystems shortly.

The Wind Resource.

Some have argued that that the available global

wind resource is considerably less that the 100 TWPE figure that

came from an extensive study about seven years ago. However, each successive

studies show the potential wind resource is even larger. The latest study

shows the global resource at 700-1200 PWhr/yr [2], while the world’s

total primary energy usage (grid, transport, industrial, residential, agricultural)

is ~150 PWhr/yr. There is sufficient point-source CO2 available

in the U.S. (over 4 Gt/yr) and sufficient wind energy potential (~80 PWhr/yr)

to synthesize

over twice the current U.S. liquid fuel usage (~0.7 Gt/yr) and supply over

twice its other energy needs (~20 PWhr/yr). The domestic wind potential is

similarly favorable in China, Russia, Canada, Australia, the U.K, Brazil,

and some other countries.

Wind Turbine Progress.

There are many opportunities for further improvements in the economics of

wind turbine manufacturing. For example, a new grade of high-strength glass

fiber has become available that should soon increase the performance per

cost of

wind turbine blades by 20%. However, the biggest single advance may be the

introduction

of

carbon-fiber-reinforced composites, which have only within the past four

years become competitive for some purposes in the automotive industry and

are not yet

being utilized in wind turbines. The production cost of commercial-grade

carbon fibers has dropped by a factor of four (in adjusted dollars)

in the past

25 years (though their market price has seen considerable volatility). The

global market in 2010 will be ~50M kg. The manufacturing cost continues

to drop and production capacity is expected to continue to increase at the

rate of 11%/yr, driven mostly by new automotive and aerospace applications.

More than a factor-of-two drop in real price (from $35/kg to $15/kg) appears

likely over the next 15 years,

and they

will soon begin being used in some wind turbines. The first large carbon-fiber

reinforced blades may be coming from Global Blade Technology within two years

using carbon fibers by Zoltek Corp of St Louis, MO.

From a distance, it is hard to get an

accurate impression of the actual size of modern wind turbines.

This close-up on the main portions of 2.3 MW Siemens blades

ready for transport helps to put them in perspective.

|

Another advance of perhaps

similar import is the ever-increasing size of the wind turbines.

The

160-m rotor diameter of the 7.5 MW wind turbines currently under

development by

Clipper is about 2.5 times the wingspan of the Boeing 747.

As the blades become longer and the towers higher, the available

wind resource increases,

as the turbines extract more energy from higher altitudes. and

yields far more energy per square mile of land.

Some of the wind turbines of a decade

ago experienced pre-mature failures because of an insufficient

understanding to the need to

limit peak stresses in composites to a few percent of the yield

limits when the part needs to withstand tens of millions of stress

cycles.

However, it is also not difficult to find examples of wind mills

that have worked steadily for 70 to 80 years. About 96% of the

larger turbines (by Bonus, a predecessor of Siemens) installed

in the mid-1980’s in California are still running well,

more than 20 years later, now with only minor annual service.

Several firms are introducing versions with direct-drive generators,

which could reduce routine service from annual to every second

or third year. As more experience

accumulates on the latest designs, we should soon begin to see

40-year lifetime guarantees; and 60-year lifetime guarantees

can be expected

within a decade.

The Clipper 2.5 MW variable-speed permanent-magnet generator

system will provide even greater cost and efficiency advantages

for WindFuels than it has for grid power.

|

The RFTS Plant.

The second biggest subsystem is the RFTS plant.

Investments in related GTL plants over the past six years have

totaled tens of billions of dollars, as huge new plants are

rapidly being built to convert stranded gas and coal into methanol and

diesel. The largest NG-to-diesel plant, for example, is being

built

by Shell in Qatar to produce 140,000 barrels of NG-GTL diesel

per day. There would be more differences than similarities between

such a plant and one for making mid-alcohols, gasoline, light

olefins, and high-value chemicals from waste CO2 and

wind energy, but there will also be a lot of common equipment requirements.

The existing

suppliers of process equipment for conventional GTL plants

will be quite capable of re-tooling to supply much of the equipment

needed for the RFTS plants at the rate needed after the design

details are worked out.

The

advances made by the automotive industry in SUV hybrid generator,

motor, and power-conditioning

technology will be of enormous value in developing the motor/generator technology

needed for the variable-speed expanders and compressors. (The power-plant

companies generally don’t like to leave their comfort

zones of steam and 50/60 Hz, and that won’t work here.)

The recuperators and condensers will utilize technology that

has already been developed by the air-conditioning

industry. There are enough international GTL, hybrid motor/generator,

and

AC condenser players, both large and mid-sized, to keep the pricing competitive.

Chemical processes, unlike agricultural processes (including growing and

harvesting of algae) are much more compatible with scale up [5]. One of the

first rules in limiting costs in chemical processes is to avoid reactions

and separations that involve a solid phase – as seen in algal oil and

cellulosic ethanol, for example. Coal-to-liquids plants typically produce

fuels at the rate of 1 billion gal/year [4]. The US market needs a supply

of 200 Bgal/yr of

sustainable, carbon-neutral fuels. Meeting even 4% of that need with cellulosic

ethanol would require over 100 Mt/yr of feedstocks, (two-thirds the current

total hay production in the U.S.), which could drive the price

of cellulosic feedstocks to $500/ton and put the price of cellulosic

ethanol at $6.50/gal.

CO2 Separations.

The third largest area from a total capital perspective for WindFuels will

be the large CO2 separation systems at point

sources (coal power plants, cement factories, biofuels refineries...) , but

like the wind turbines, this too will be independent of the RFTS plants.

As explained on the CO2market page,

the RFTS plant will simply purchase CO2 on the

rapidly expanding open market.

There has been strong support

by many governments (including the U.S. DOE)

and oil companies over the past

five years for reducing the cost of CO2 separations

at power plants, and this will bring separation costs down considerably

over the next five years.

The processes being developed for CO2 sequestration

are aimed at about 97% CO2 purity, as currently

used in large quantities in enhanced oil recovery (EOR). The additional

purification needed for WindFuels

will be straightforward and not very expensive. The WindFuels plants will

create

an

enormous

market for CO2. An extensive CO2 pipeline

infrastructure is already beginning to be built for immediate needs in EOR

and soon for

sequestration. See the Physical

CO2 Market for more information.

Electrolyzers.

After the wind turbines, the next largest

subcontracted “component” is

the water electrolyzer. (The RFTS plant and the CO2 separation

processes at the

coal plants are not “components” in the normal sense of this

word.) Commercially available electrolyzers above the 250 kW level have

been achieving 73% HHV efficiency for the past

8 years, and steady progress has been made in oxygen-evolving catalysts

and electrolyte formulations. Commercial products are available at least

to the 2.2 MW level. Alkaline electrolyzers have demonstrated HHV stack efficiencies

of 92% at low currents and 84% stack efficiency at full power; and PEM electrolyzers

have demonstrated low-current stack efficiencies up to 95%, though they are

still quite expensive. Moreover,

we have shown in a pending patent how it is possible to convert the waste

heat from electrolyzers to electricity much more efficiently that has previously

been thought possible.

Water usage by a WindFuels plant will be at least an order of

magnitude less than needed for nuclear, shale oil, or biofuels.

The WindFuels

simulations carried

out thus far have all assumed dry cooling. Supplying the needed pure water

for the electrolyzer will not be a problem even in areas where

water shortages occur,

as there has been enormous progress in reverse osmosis (RO) water purification

over the past decade. The cost of removing 99.8% of the salts and other impurities

from seawater (or other water resources of similarly poor quality) will soon

be under $0.1/ton. The water purification membrane industry now exceeds $4B

and is growing at about 8% annually. The additional cost of getting

the water purity

needed (de-ionized) for the electrolyzer from RO-quality water is minor.

Alternatively, methods can be implemented to utilize double-RO

water in the electrolyzer.

Sustained Scale-up.

Some of the oil, gas, and coal companies may not be sufficiently motivated

to help develop a tough, new, competing industry. Unfortunately, the kind

of approach we have generally seen at the DOE for the

past 3 decades will also not work. Without a complete transformation,

oil prices could be over $1000/bbl in 15 years.

The wind turbine, chemical, air conditioning,

and other established industries can play major roles in the

new RFTS industry. But success will depend even

more

crucially on new, highly sophisticated, RFTS general contractors with the

expertise needed to manage the new developments and bring all the components

together cost

effectively.

References:

1. Nancy Spring, “Turbine Tech Drives Wind into the Generation

Mainstream”, Power Engineering International, Nov., 2008.

http://pepei.pennnet.com/display_article/346401/6/ARTCL/none/none/1/Turbine-Tech-Drives-Wind-Into-the-Generation-Mainstream/

2. X Lu, MB McElroy, and J Kiviluoma, “Global potential

for wind-generated electricity”, PNAS, 10.1073, 2009.

3. R Wiser, M Bolinger, “Annual Report on US Wind Power

Installation, Cost, and Performance Trends: 2007”, DOE-EERE,

http://www1.eere.energy.gov/windandhydro/pdfs/43025.pdf.

4. AP Steynberg and ME Dry, eds. Studies in Surface Science and

Catalysis 152, Fischer-Tropsch Technology, Elsevier, 2004.

5. K Weissermel, HJ Arpe, Industrial Organic Chemistry, 4th

ed., Wiley, 2003.

6. K Ibsen, “Equipment Design and Cost Estimation for

Small Modular Biomass Systems. Task 9: Mixed Alcohols from Syngas – State

of the Technology”, NREL/SR-510-39947, 2006. http://www.nrel.gov/docs/fy06osti/39947.pdf

7. PL

Spath and DC Dayton, “Preliminary Screening – Technical

and Economic Assessment of Synthesis Gas to Fuels and Chemicals

with Emphasis on the Potential for Biomass-Derived Syngas”,

http://www.fischer-tropsch.org/DOE/DOE_reports/510/510-34929/510-34929.pdf , NREL/TP-510-34929, 2003.

8. JR Hensman, D Newton, “Fischer-Tropsch Synthesis Process”,

US Pat #7,115,670, 2006.

9. AP Steynberg, JW De Boer, HG Nel, WS Ernst, JJ Liebenberg, “Process

for Synthesizing Hydrocarbons”, Pending Pat. appl. pub.

US 2007/0142481.

10. G Olah and A Molar, Hydrocarbon Chemistry, 2nd ed., Wiley,

2003.

11. TL Brown, HE LeMay, and BE Bursten, Chemistry, the Central

Science, 10th ed, 2005, Prentice Hall.

12. CH Bartholomew and RJ Farrauto, Industrial Catalytic Processes,

Wiley, 2006.

13. JD Seader and EJ Henley, Separation Process Principles, 2nd

ed., Wiley, 2006.

14. J Ivy, “Summary of Electrolytic Hydrogen Production”,

NREL/MP-560-36734, 2004, http://www.nfpa.org/assets/files/PDF/CodesStandards/HCGNRELElectrolytichydrogenproduction04-04.pdf

15. JI Levene, “Economic Analysis of Hydrogen Production

from Wind”, WindPower 2005, Denver, NREL/CP-560-38210,

2005. http://www.nrel.gov/docs/fy05osti/38210.pdf

16. DESIGN II for Windows Tutorial and

Samples Version 9.4, 2007, by WinSim Inc., available from http://www.lulu.com/includes/download.php?fCID=390777&fMID=810115 .

17. FG Kerry, Industrial Gas Handbook – Gas Separation

and Purification, CRC Press, Boca Raton, 2007.

18. http://www.nrel.gov/wind/advanced_technology.html

19. http://www.wwindea.org/home/index.php

20. Wind turbine service records, http://www.renewableenergyworld.com/rea/news/article/2009/08/keep-the-blades-turning?cmpid=WNL-Wednesday-August26-2009

21. K Harrison, G Martin, T Ramsden, G Saur, “Renewable

Electrolysis Integrated System Development and Testing”,

NREL PDP_17_Harrison, 2009, http://www.hydrogen.energy.gov/pdfs/review09/pdp_17_harrison.pdf .

22. MW Kanan and DG Nocera, “In Situ Formation of an Oxygen-Evolving

Catalyst in Neutral Water Containing Phosphate and Co2+”,

Sci., 321, 1072-1075, 14 Sept., 2008.

|

|

| |

| No other renewable resource has come close to the competitiveness

and scalability of wind other than hydro – and hydro

is nearly tapped out. |

| |

| There is sufficient U.S.

potential wind energy (80 TWhr/yr) and point-source CO2 (4

Gt) in the U.S. to produce twice the current domestic liquid

fuel usage and all its other energy needs. |

| |

| The mean

price of wind turbines in the U.S. dropped from $1600 to

$1300/kW since

2008.

Chinese wind turbines are now being quoted at under $800/kW

(installed) in many places around the world.

|

| |

| If wind

maintains the growth rate it has demonstrated over the past

15 years for another 10 years, it could then be

larger than the automotive industry. |

| |

| About 20 TWPE will be required to replace 60% of global

fossil oil and gas usage with WindFuels.

That is doable within 35 years. |

| |

| The WindFuels

industry will remain vibrant for centuries. |

| |

| Carbon

fiber composites should soon permit more cost reductions

in wind turbines. |

| |

| Wind

receives much less federal grant money than

solar, but wind is adding new capacity

an order of magnitude faster. |

| |

| Much of the equipment needed in the RFTS plants will be

similar to that used in current GTL plants, power plants,

and in the air-conditioning and jet-engine industries. |

| |

| We’ll need

about 5000 250 MW WindFuels plants to meet all our (US) oil

and gas import needs today. By 2035, we’ll

need about 8,000.

8,000 is not such a big number. Each of these plants should

fit on about twenty acres.

|

| |

| For more details on the

plant design and analysis, see RFTS Detailed Design 1.0. |

| |

| The DOE

is currently supporting a 1 MMT CO2 separation

demonstration for $300 million. One 250 MW WindFuels would

offset that amount of CO2 in only two

years. |

| |

| Scale-up of the alkaline-type water electrolyzers will

be straightforward. |

| |

Tax breaks don’t work. They don’t help start-ups

that aren’t making money.

It will take huge grants to innovative, highly motivated

start-ups.

It got us to the moon in a decade. It can now give us

carbon-neutral energy security in three decades.

|

| |

|

|

|